Analysts Are Getting Worried About the Euro

It’s 2007 all over again.

The euro is on a tear, U.S. investors are snapping up European stocks — and traditional theories to justify the shared currency’s spirited advance have broken down, as investors luxuriate in a climate of low volatility.

That’s the market landscape as painted by Deutsche Bank AG strategist George Saravelos. Given the parallels, he suggests caution after the euro’s 7 percent rally against the dollar this year.

“Something strange has happened to the euro in recent months,” Saravelos wrote in a client note Wednesday. “Almost all traditional drivers that usually ‘explain’ the price action have broken down.”

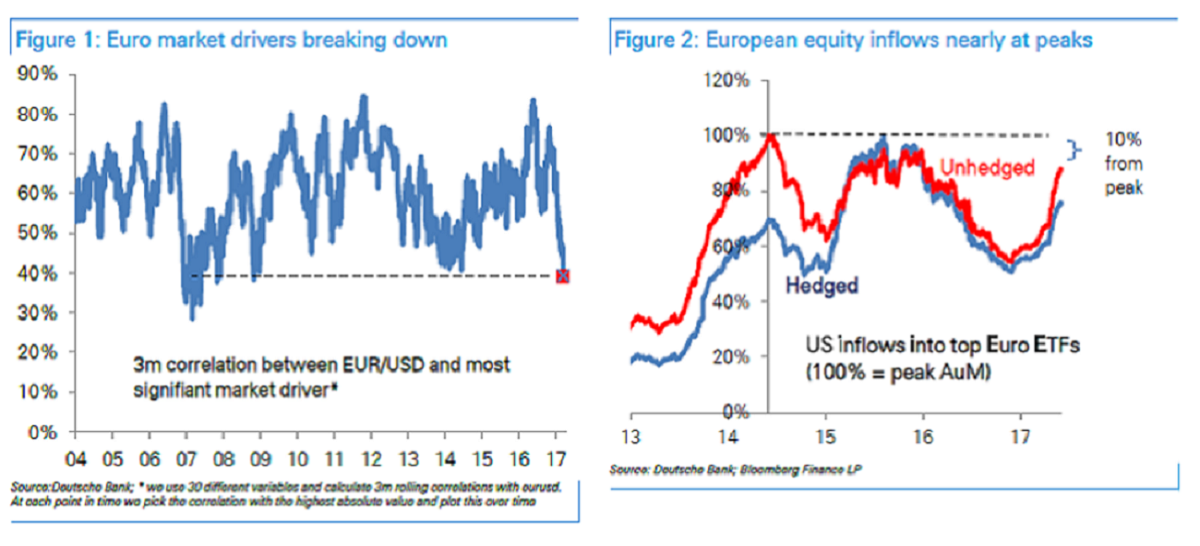

The bank’s currency correlation model — which includes factors such as interest-rate differentials, the relative performance of equity markets, and spreads of southern European government bonds — is flashing red.

Correlations between the euro’s rolling three-month performance against the dollar and other such factors were last at current subdued levels in early 2014 and 2007. That suggests unhedged equity inflows from foreign investors piling into European equity and bond markets — thanks to better-than-expected economic data, and easing political risk — have driven the currency’s recent outperformance, according to Deutsche Bank.

“Near-term, it suggests that there may be an underlying flow story that is impervious to other market drivers and is supportive of the euro,” Saravelos said. “Medium-term, the current ‘decorrelation’ is usually associated with periods of very low volatility and would suggest caution in extrapolating recent euro strength.”

As such, the German bank, the world’s fifth-largest currency trader by market share according to a Euromoney Institutional Investor Plc, reckons the euro will fail to break out against the top end of its 1.05 to 1.15 per dollar range, as traditional currency drivers re-assert their influence.

Risks to the currency’s bull run are rising: The euro fell 0.2 percent Wednesday after a Bloomberg report on a potential switch in the European Central Bank’s inflation outlook signaled a dovish outcome in a policy decision due Thursday. The euro was flat at $1.1260 ahead of the ECB meeting.

The counterpoint comes from Morgan Stanley, which this week raised its target for the single currency citing “material upside surprises in recent growth data, positive political developments and a view that investment inflows to the eurozone will continue.”

Morgan Stanley projects 1.16 per dollar by the second quarter of 2018, a 20 percent upside from its previous forecast, compared with the median projection of 1.13, according to analysts surveyed by Bloomberg.

Linking currency moves to capital flows isn’t straightforward when markets move in lockstep, but an April study by Deutsche Bank suggests currency traders should follow flow data closely: It concluded that outsize inflows into exchange-traded equity funds can predict moves in a number of liquid currencies, including the euro.

Saravelos’s note of caution also finds support from Jens Nordvig, founder of Exante Data, a New York-based research firm.

“Fundamental models for EURUSD, based on rate differentials, would have predicted a relatively stable exchange rate in recent months,” Nordvig, who was ranked No. 1 strategist by Institutional Investor for five years through 2015, in his previous capacity as head of currency research at Nomura Holdings Inc., wrote in a client note. “In our analysis, this ‘euro residual’ is tied to certain flow forces, which have turned euro bullish lately.”

Source: Bloomberg.com